")

")

Impact of Oil Price Shocks on Macroeconomic Performance: A case study of oil-exporters.

Chapter 1: Introduction

1.1 Study background

The volatility of crude oil price has been experienced since the end of the 20th century. The March 1999 spikes were experienced due to the restriction of crude oil production and cooperation among OPEC member states, the growth of oil demand in Asia that signified its recovery following the Asian financial crisis, and decreased production from non-OPEC countries (Al-Abri, 2013). There were sharp increases in the price of crude oil to the tune ofmore than$30 per barrel in the last quarter of 2000 (Chen, Hamori and Kinkyo, 2014). OPEC countries tried to stabilize the prices through increasing or reducing production in the range of $22 per barrel to $28 per barrel (Ghosh and Kanjilal, 2014). In September 2001, due to the 9/11 attacks,there was a deep reduction in the price of crude oil, irrespective of earlier decreases in production of oil bynon-OPEC exporters and quota reduction by OPEC countries. After a short while, prices rose to $25 per barrel with prices going beyond this in 2004 to about $40 per barrel (Jimenez-Rodriguez, 2011).

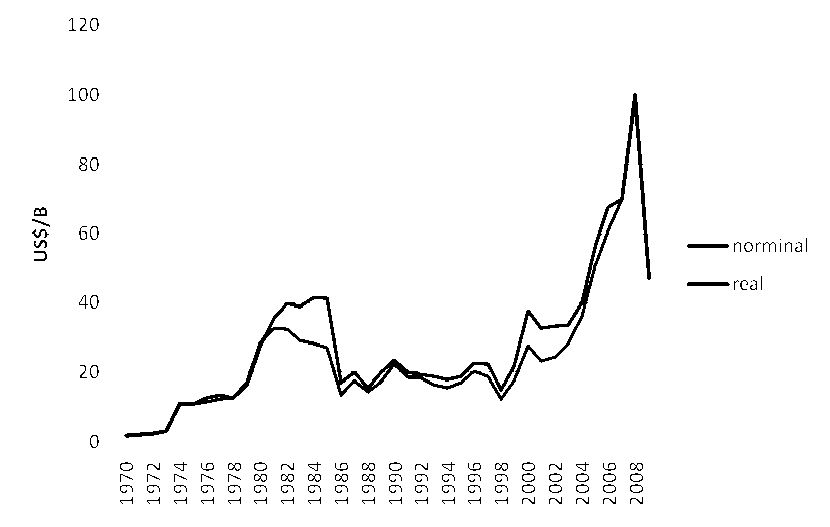

Factors linked to the rise in the price of oil include the continuous devaluation of the USD,tensions in the Middle East, China’s increased demand for crude oil and the uncertainty of oil production in Russia (Chuku, 2012). The 2008 banking crisis, a consequence of the financial crisis, reinforced significantly the cyclical downturn. After the insolvency of numerous financial institutions and banks in the US, Europe as well as developing countries, the financial conditions tightened. The resulting economic meltdown led to an oil price crash. The movements in the price of crude oil are illustrated in the figure 1.1.

Figure 1.1: Real and nominal oil price movements between 1970 and 2008 Source: OPEC

According to Kilian (2009), the price of oil was below $100 per barrel in 2008 and rose to $140 per barrel midyear and by the end of the year; the price was considerably below $40 per barrel with changes occurring almost weekly. In 2011, the prices were between $85 per barrel and $110 per barrel. This volatility has been linked to the fact that markets many times overprice since they are not perfectly efficient. Nevertheless, Jiménez-Rodríguez and Sánchez (2012) argues that underlying economic bases in themselves result in complex price dynamics. Bernanke, Gertler and Watson (2004) point to a projection of the Energy information Administration’s (EIA) that predicts that by 2035, the volatility of crude oil prices will continue with the highest price going up to $235 per barrel.

The relationship between the price of oil and economic output has been identified for all recessions with the exception of one from the beginning of 1950 (Jiménez-Rodríguez and Sánchez, 2012). Oil price shifts have the capability of affecting the economy by means of numerous channels including a rise in production costs, uncertainty in investment, inflation and wealth transfer.

Even though traditionally, scholars have emphasized the general effect of oil shocks on the economic output, Bjørnland (2008) indicates that the relation of oil price movements and economic output vary depending on the source of the movement of the price of crude oil. An oil price shock, being the disruption of production in economies that export oil is linked with lower levels of production and as a consequence, higher prices of oil which causes inflation and the depression of world economic activity. The price of crude oil is also likely to rise as a result of enhanced global activity or motives that are precautionary. Economies that export oil react to enhanced global activity through either exploring new resources or increasing the price of crude oil. Now should the source of the price increase be precautionary measures, there may be increased output as a result of the resource shift for oil exporting countries. Nevertheless, a section of the income transferred to countries that export oil is likely to be recycled through a rise in trade, which reduces the negative consequence on output caused by particular demand shock.

1.2 Statement of the problem

Some of the models that study the macroeconomic effects of oil price shocks assume that oil price shocks arise from fluctuations in supply and are exogenous to aggregates in economic output. These assumptions have resulted in varied degrees of significance as pertains to macroeconomic effects. For instance, Guidi (2010) in a study reports findings that indicate that factors excluding oil price shocks led to the recessions in the 70s, for instance, systematic monetary reactions to the shocks. However, Ali, Huson and Wadud (2011) find that the major cause was the oil price shocks by modifying the model in the previous study.

With the differences in the results of varied scholars, there is need to establish the real effects of oil price shocks on economic output and particularly in the period spanning the 80s to the most recent times. There is also need to examine this from the perspective of oil exporters and not importers given that volatility of the crude oil price for importers is well documented from the multiple studies conducted in the area.

Additionally, given that not many researchers have examined developing countries, for instance, African oil exporting economies, there is need to examine the macroeconomic effects of oil price shocks in this region. The studies that have investigated African countries have concentrated on the period preceding the financial crisis of 2008 and shortly afterwards leading to the need for an updated study. It is important to undersand the significance of the financial crises of 2008. The 2008 financial crisis was a global financial crisis which severly impacted the economy of almost all the nations. Considered to be the worst financial crisis since the Great Depression of 1930s, its impact was felt around the globe. The oil process which were spiraling upwards for the preceding 6 years, went down significantly, from the highs of $ 147 per barrel to the levels of $ 40 by the end of 2008. This sudden reduction in prices and subsequent effect on the economies of the oil exporting countries resulted in slowing of economic growth of many emerging oil exporting nations. It forced them to draw down the reserves and cut down on investments. The financial crisis of 2008 therefore had a major impact on the Macroeconomic performance of these nations.

Moreover, the majority of the African oil exporting nations experience war, which could be a contributor to changes in economic output and therefore, a cross country examination of output versus oil price shocks with control factors, such as, inflation and short term interest rates would help in eliminating country factors thereby giving need for the investigation of the same. Similar effects have been felt by the oil exporting nations from middle East, however to a lesser extent vis-à-vis African nations. The increase in the process of oil has resulted in transfer of capital to the oil exporting nations. Due to lower absorption capacity of these nations, the capital transfer does not get converted to higher imports, thereby resulting in higher savings for these nations. This has been observed in the cases of United Arab Emirates, Qatar, Kuwait and Saudi Arabia. Similar to African nations, the Persian Gulf and rest of the Middle East have been in a state of turmoil and this factor also significantly contributes to oil price shocks.

The oil prices and the Macro- economy are co- related. The changes in the price of oil affect the Macro- economy of a nation in a significant manner. A rise in the prices of oil results in higher cost of transportation, which further results in inflation, lower savings and subsequently leads to slowing of the economy of a country. The oil prices have a high co- relation with a country’s Gross National Output and Gross Domestic Product. Many major oil exporting emerging economies of Africa and Asia have a great dependency of the prices of oil. Oil export contributes significantly to the economies of these countries. However, this relation between oil prices and macro- economy is asymmetric. An increase in the prices of the oil have a larger impact on the macro- economy as compared to the impact of the reduction of the oil prices on the macro- economy.

1.3 The research aim

The aim of this study is to investigate the impact of oil price shocks on economic output of oil exporting African countries. The study analysis various researches conducted by several scholars and infer the resultant impact of oil price shocks on the macro- economy of nations in a coherent manner while simultaneously trying to identify the specific co- relating elements between the oil prices and economies of countries.

1.4 Research objectives

- To investigate the current trend of oil price movements. This involves analysing the impact of movement in oil prices in not just historic perspective but also the current variables impacting the oil price movements and the resulting effect over the macro economy. This is important because of the fact that the Global Financial crisis of 2008 is relatively recent is the worst in history since the Great Depression of the 1930s. Further, the volatility in the global economy still persists and political tensions and turmoil continue to affect the oil exporting African as well as Middle East countries. The need to investigate oil price movements from a contemporary perspective is therefore logical as well as relevant.

- To investigate the relationship between oil price shocks and macroeconomic performance for African oil exporters

1.5 Rationale

After the financial crisis, the consumption of oil in developing countries went beyond that of the US. The increases in the demand for oil in developing markets coupled with the depletion of supplies contribute to the significance of the research on oil prices in emerging markets. This is especially true for African emerging markets that are exporters of oil. As such, this research contributes to emerging markets literature in two ways. First, this research examines the economic output of oil exporting developing countries in Africa, the majority of which are experiencing war in varied degrees, thereby helping in the identification of whether the changes in output are a result of oil price shocks or other exogenous variables.

Secondly, the study includes money supply, interest rates and inflation as moderating factors across countries. This makes the study unique in comparison with previous studies. The study also employs the tested and recommended method by renowned researchers in this field, the VEC model. This ensures that the results are dependable thereby contributing significantly to the literature. The results of the study will additionally be useful to governments of emerging economies in their decisions during and after an oil price shock through the understanding of the impact of those decisions on their economies.

1.6 Hypothesis

Oil price shocks have a long-term cyclical effect on the GDP of developing African oil exporters.

1.7 Structure of remaining chapters

The remaining chapters comprise the literature review, whereby, the theory of investment under uncertainty and its link to the relationship between oil price shocks and economic output are discussed. Also, a preview of the various studies that have been conducted in this field is given. The methodology chapter is next where there is discussion of the research philosophy adopted, the research design, the strategy for the research, the method of data collection, the validity and reliability of the methodological process, and the limitations of the research.

Followed by this is the section of results in which the outcome of the various analyses used and their implication are presented. The findings are further compared to previous findings leading to a conclusion. In the conclusions and recommendations chapter, the aim and the objectives of the research are revisited, examining whether they have been fulfilled. Additionally,the challenges experienced during the research processes are addressed and recommendations for future research are made.

Chapter 2: Literature Review

In this chapter, the literature that relatesto the relationship between oil shocks and macroeconomic performance is examined. Particularly, there is discussion on the theory of investment under uncertainty, the transmission mechanisms of oil price shocks into the economy and finally critiques of the empirical studies that have been conducted in this area of research.

2.1 Theory of investment under uncertainty

This theory concerns the behavior of investors in the setting of uncertainty. Guidi (2010) argues that uncertainty concerning the return on investment because of, for instance the prices of energy may result in the creation of cyclical fluctuations in investments. The effect comes into play from a company’s joint decision of where and when to commit resources among the irreversible investments. The uncertainty regarding future return on investment stimulates optimizing agents to delay investment for the period in which the expected additional information value is greater than the short term return expected to current investment.

With the perseverance of uncertainty, the tendency of companies to commit their investible resources becomes higher. The impact of uncertainty on the decisions of whether to commit resources or not, is similar to the effect of uncertainty on decisions regarding the exercising of a call option on financial assets that pay dividends. The rise of uncertainty regarding the return of the underlying financial asset has the tendency of delaying the decision to exercise. As such, uncertainty may result in diminishing the willingness of companies to commit their resources to irreversible investments and in the same way the willingness of buyers to spend on durables that are illiquid. This gives the suggestion that, for instance the uncertainty concerning the prices of oil has the likelihood of resulting in auto manufacturers delaying decisions regarding the commitment of resources to the development of luxury vehicles and has the similar likelihood of causing the buyers to delay their decisions regarding the type of vehicle to purchase.

Bernanke, Gertler and Watson (2004) present the argument that investment decisions at the micro level, such as that, have the capability of resulting in macro-level fluctuations. The first main reason is that the macro-economy may not have sufficient diversification from particular large industries, such as the automobile industry, to make the economy immune from fluctuations at industry level. Secondly, when information is imperfect, agents may not have the certainty regarding the permanence of the first shock to the investment, which converts a transient shock into a disturbance that is more volatile.

Ghosh and Kanjilal(2014) argue that uncertainty in the price of oil has the capability of resulting in a similar scenario. The rise in oil prices has the capability to imply a classic shock on the side of supply, which leads to a reduction in potential output. The rising prices of oil signal the increase of energy scarcity, which is a fundamental input in production. As a consequence, output growth and productivity decelerate. The deceleration in the growth of productivity leads to a decrease in the growth of wages and increase in the rate of unemployment at which inflation accelerates. In the case that consumers expect the increase in the price of oil to be temporary, they have the tendency of smoothing out their consumption through less savings and increased borrowing that leads to a rise in the equilibrium real rate of interest. As the growth in output decreases and real rate of interest increases, there is a fall in the demand for real cash balances and for a certain monetary aggregate growth, the inflation rate rises. The rise in oil prices as a consequence leads to a reduction in the GDP growth rate, while boosting the real rate of interest and measured inflation rate.

2.2 The transmission mechanisms of oil price shocks in the economy

According to Chuk, (2012), the transmission mechanisms of oil price shocks into the macro economy are three: aggregate supply, aggregate demand,and the structure of interest rates. In the mechanism of aggregate supply, Morana(2013) realizes that the impact on producers can provide the explanation concerning business cycles from petroleum price shocks and technology. This means that energy price increases result in an imperfect competition structure of the market where the pricing of goods by firms goes beyond the marginal cost. In an imperfectly competitive market structure, energy price shocks would lead to the reduction in capital use leading to the conclusion that in the case that the transmission mechanism of oil into GDP is through aggregate supply, the effects would be the rise of inflation.

In aggregate demand, Bjørnland(2008) explains the manner in which an increase in oil prices results in the reduction of consumers’ purchasing power, thereby, reducing expenditures on products and services. In particular, Guidi(2010) indicates that an increase in oil prices has a negative impact on output through the reduced consumption of products that are durable.

Lastly, Ushie, Adeniyi and Akongwale(2012) explain that in terms of the interest rate structure, the transmission mechanism comes through the systematic response to monetary policy. A positive shock on the price of oil has the tendency of raising the inflationary expectations of the public, steepening treasury securities’ yield curve, pressuring the rise of the target for governments’ fund rate and ultimately slowing down the economic growth. Economic fluctuations are therefore not seen as resulting directly from oil price shocks.

Even though the mechanisms of transmission have a contribution towards the understanding of the manner in which oil price shocks impact the economy, no consensus exists in terms of which one of them dominates(Filis and Chatziantoniou, 2014). Additionally, the mechanisms may lose their relevance due to the decline in the effect of oil price shocks(Chen, Hamori and Kinkyo, 2014). Also, the effect of the shocks on the fluctuation of the macro-economy differ depending on the cause of the shocks and therefore, the mechanism of transmission will depend on the prominence of the underlying cause(Kilian,2009).

2.3 Early empirical studies on oil price shocks and macroeconomic performance

Numerous studies have been conducted in the last 30 years regarding the effect of oil price shocks on the macroeconomic performance. According to Bjørnland (2008), oil price shocks versus macroeconomic studies were pioneered by Hamilton in the 80s, a period preceded by very high increases in the price of oil. In his study, the scholar realized that the majority of the recessions in the US before the 1972 had prior increases in the price of oil. The phenomenon was explained by use of three hypotheses, stating that the correlations gave a representation of historical coincidence, that they were the result of endogenous variables that could be explained which have effects on both series and that at least some of the US recessions had their cause in the exogenous rise in oil shocks.

The model presented by Hamilton rejected the first two hypotheses, but accepted the third given that between 1948 and 1980, the results revealed a significant relationship between the real GNP of the US and oil prices. This relationship was extended by Morana (2013) into the 80s and realized that the significance was weaker.

Nevertheless, in the case that the negative and positive oil price shifts were regarded as different variables, the former maintained statistical significance. This gave the suggestion that output and oil prices are attributed to an asymmetric relationship where decreases in oil prices do not have as substantial an effect on the macroeconomic variables and in some cases may produce a negative effect.

In a study carried by Hooker in 1996, the relationship between oil prices and output according to Jiménez-Rodríguez and Sánchez (2012) was found to have weakened in the 80s. The results indicated that the oil prices did not Granger-cause a majority of the economic variables for instance, GDP when examining the period ranging from 1973 to 1995. Even following corrections made on the asymmetric link between the prices of oil and output, the Granger causality still failed. In a later study, Hamilton reacted to this study by accepting the findings while disagreeing with the manner in which shocks to prices were treated(Hamilton and Herrera, 2004). The argument was that given that the majority of oil price increases had been preceded by an even larger decrease in oil prices, the examination of quarterly oil prices meant that the volatility in oil prices was more than the actual volatility. Hamilton nevertheless agreed that consumers would feel the effect of yearly changes in the prices of products, therefore, the oil price shocks need to make comparisons between the current price and the previous year’s price.

The observations made by Mork on the asymmetrical association between output and oil prices were succeeded by numerous studies that attempted to provide explanations for the same. According to Hamilton, the asymmetry was due to the uncertainty in the supply and price of oil that resulted in firms and individuals to postpone their decisions to invest. This implied that the decrease of oil price would have mirror effects compared to the increase in oil prices. Kilian (2009) realized that oil price shocks had effects on economic activity through sectorial shocks and channels of uncertainty. The mechanisms gave the suggestion that changes in the oil price had impacts on the price of products in industries that are energy intensive for instance consumer durables through the shifts in cost structures.

2.4 Recent studies on oil price shock and macroeconomic performance

In a study carried out by Al-Abri(2013) in which the scholar investigated the effect of exchange rate regime on the relationship between oil price shocks and macroeconomic performance, the findings agreed with Friedman’s hypothesis that only real exchange rates and consumer prices change faster and smoothen in the long run. The panel Granger causality tests provided the suggestion that there exists a feedback from the real rate of inflation and effective rates of exchange, thereby supporting the argument that oil price shocks in developing countries may not be solely exogenous. The research used consumer prices, real output, real exchange rates and interest rates with the sample comprising OECD’s major oil importing economies.

This research did not focus mainly on examining the effect of oil price shocks on macroeconomic performance, although panel Granger causality tests were used to describe the relationship. The results also do not give an indication of the long-term and short-term effects of oil shocks on the macro economy and whether the effects lead to increased or decreased output. Also, the study solely examined oil importing countries which according to Gómez-Loscos, Gadea and Montañés(2012), have a different reaction to oil shocks compared to oil exporting countries.

Jiménez-Rodríguez and Sánchez (2009) combined both linear VAR and three nonlinear approaches, including Mork’s asymmetric model, Lee’s scaled model and Hamilton’s net oil model in their estimation of the effects of oil price shocks on the real economy of major industrialized OECD economies. The scholars used quarterly data between 1970:3 and 2003:4 with variables including short-term interest rate, the real wage, long-term interest rate, CPI inflation, real effective exchange rate and real wages. The results showed that there exist non-linear impacts of the price of oil on inflation and the real economy. Additionally, the researchers revealed that when the conditional variance of the shocks was controlled, the context of oil price volatility became of importance with those having stable price environments exhibiting larger impacts compared to those having a fluctuating price environment.

Although this study used a number of models that focus on the effect of oil shocks on macroeconomic performance, thereby seeming to integrate all of them, the period of sampling according to Ghosh, Varvares and Morley (2009) exhibited decreased volatility of oil prices with diminishing effects on output. Therefore, this may not give a reflection of the current behavior of the macro economy. The scholar additionally did not indicate whether the economies chosen are importers or exporters of oil and therefore does not provide clarity in terms of the differences in behavior of output of the oil importing and exporting economies.

A more precise study was carried out by Ghosh, Varvares and Morley, (2009) in which the researchers focused on the effect of oil price shocks on the macro economy of the US using two of the Hamilton’s models. The scholars settled on a structural error correction model, which enabled the changes in the oil price to have effects in the short and long run. The preferred model suggested that the price of oil led to a reduction in the growth of GDP by approximately 0.4% in the first, second and third quarters of 2008 and an increase of 1.7% in the fourth quarter of 2008 as the prices of crude oil fell. This study was conducted on an oil producing country (the US) whose results may be close to the effects of the oil price shocks on major African oil producing countries. Nevertheless, the study does not provide long run effects of the oil price shocks on the performance of the macro-economy. Moreover, the study seems to concentrate on the effects only within 2008.

In another research conducted on an oil producing country (Japan) with the time ranging from between the first quarter of 1976 and the second quarter of 2008, Jiménez-Rodríguez and Sánchez, (2012) used a modeling technique that helped incorporate information concerning structural breaks in the variables used. The purpose was to represent the channels of transmission of oil price shocks into the macro economy. The results indicated that oil price shocks resulted in a reduction of industrial production and increased inflation. Nevertheless, the effects were only shown to be evident between the late 70s and early 80’s. This result additionally did not show the long run effects of oil price shocks on the macro economy.

The studies discussed so far were carried out in developed economies either in America, Europe or Asia. Further, all the studies seem to incorporate only countries that are members of the OECD. According to Iwayemi and Fowowe (2011), the results may differ from one country to another, depending on whether the countries are developed or developing. Further, Ali, Huson and Wadud(2011) indicate that given that any economic cooperation often seeks to integrate economic policies among member states, there is a need to examine studies from other countries not within the economic zone and particularly those carried out among African countries.

Umar and Abdulhakeem (2010) carried out such a studyon the effect of oil price fluctuations in Nigeria. Using the VAR model, the results revealed that oil prices greatly affect GDP, unemployment and money supply with the impact on price index not being regarded as significant. The conclusion arrived at is that given the volatility of the economy to external shocks, the macroeconomic performance is also volatile thereby bringing about difficulties in macroeconomic management.The researchers do not indicate whether the effect is negative or positive and whether the volatility pointed to is only short run or extends to the long run. Furthermore, the study does not cover the more recent price movements that occurred during and after the financial crisis.

Another research carried out byBerument, Ceylan and Dogan (2010) on the impact of oil price shocks on the economic growth of specific Middle East and North African countries regarded as being either net importers or net exporters. The researchers used the VAR model with the results indicating that the increase in oil prices positively and significantly affects the outputs of Algeria and Libya but have no statistically significant effect on Egypt, Djibouti, Morocco and Tunisia. The variables considered included the real exchange rate, GDP and inflation with data collected from 1952 -2005. This study also does not include the most recent price shocks and although it shows that the effects are positive for certain countries, an explanation is not provided for the non-significance of the results in other countries.

Lastly, Iwayemi and Fowowe (2011) carried out a study on the effect of oil price shocks on the macroeconomic performance of oil exporting countries such as Libya, Nigeria, Algeria and Libya by using the VAR model. The data were collected over a range of 35 years from 1970 to 2006. From the Granger causality tests, the researchers find that there are no short run effects and that the IRF reveal that oil price shocks leads to volatile responses on the macroeconomic variables with initial responses being negative the explanation given for this finding is that the extra earnings during oil price increases are not channeled into economic development. The macroeconomic variables considered included the CPI inflator and real GDP. The data in this research does not include the recent shocks just like the two studies observed.

From the studies on African countries indicated, there are certain weaknesses that are similar across the studies and which introduce gaps in the oil price shock research. The first, the data collected is not updated and thus does not include the most recent shocks that came with the financial crisis. Numerous scholars as observed in the literature have agreed to the weakening of study results with time. This means that the results obtained in these studies may not be similar to the ones obtained following the examination of the recent oil price shocks. Secondly, the researchers used the VAR model, which ought to be employed with the absence of unit roots. Nevertheless, economic data as observed by reference always contain unit roots, rendering the results economically meaningless. All the authors did not show evidence of unit root tests carried out in the choice of the model.

Also, even with the use of the same model, all the three studies reveal different results. While the first does not indicate whether the relationship between GDP and oil price shocks is positive or negative, the second indicates positive relationship and the third negative relationship. This is despite the fact that the second and the third studies consider similar countries. This variation in the results could be due to the use of an inappropriate model. In the last place, the researchers do not explain different ways in which the governments intervene during the oil price shocks and how that intervention affects other related macroeconomic variables. The current research addresses these disparities through the use of tests to evaluate the appropriate model. Further, it includes a wide range of independent variables such as money supply, real interest rates, inflation and GDP. While money supply and real interest rates can be controlled, the rate of inflation and real GDP are the results of the control measures and oil price shocks thereby enabling the study of changes in the control variables in order to establish government interventions.

Most of the studies discussed above have certain gaps in the conclusions drawn upon the research conducted by them respectively. In the study carried out by Al- Abri (2013), there is no clear demarcation between the long- term and short- term effects of oil price shocks and the study is limited to oil importing nations. Similarly the study carried out by Jiménez-Rodríguez and Sánchez (2009) also does not differentiate between the importers and exporters and the data used pertains to an earlier period and does not give a clear indication of the current effects of oil price shocks on the economy. Likewise, the study conducted by Ghosh, Varvares and Morley (2009) analysed the effects of oil prices on instances prior to 2008 and does not dwell into the analysing the long- term effects. In some of the other studies, like the ones conducted by Jiménez-Rodríguez and Sánchez (2012), the studies aare carried out in developed nations and therefore same conclusions cannot be drawn for developing nations of Africa.

It is therefore logical and pertinent to analyse the effects of oil price shocks on the economy in terms of short term and long term effects as well as to analyse the effects of recent times. Also, equally important is the fact to have a contextual approach while analysing the effects on the economies of different countries. Similar approach cannot be used to study the effects on the economies of Africa and other developing nations.

Chapter 3: Methodology

This chapter discusses the research philosophy and the design used to carry out the study. More specifically, the research approach used, the research strategy, time horizon and the method of data collection, and the methods used.The research follows Saunders presentation of the research methodology. Lastly, the econometric model used in the research is presented.

3.1 Research philosophy

Positivists hold the belief in the stability of reality and the ability of one to observe and describe it objectively, without interfering with the phenomenon under examination (Du and Kamakura, 2012). According to the positivists, the phenomenon ought to be isolated and the observations made have to be replicable. This involves manipulating reality while varying one independent variable for the purpose of identifying consistencies in the link between the elements constituting the social world (Hoe and Hoare, 2012). The predictions are made on the basis of realities that have been observed and explained previously as well as their interrelationships (Barnham, 2012). This philosophy fits well with the positivist beliefs and assumptions given that intent is to establish the relationship between oil price shocks and macroeconomic variables and the research is based on some previously performed studies illustrating the existence of such a relationship.

3.2 Research approach

In line with the positivist philosophy, this research adopts the deductive approach in which data is collected in measured values and the relationships mentioned in the positivist philosophy determined by statistical means. Further, in the deductive approach, it is necessary to have certain predictions of the outcome also referred to as study hypotheses, which are derived from the previous works. In this study it is hypothesized that the asymmetric and declining effect of oil negatively affects the GDP of developing African oil exporters, thus justifying the suitability of the approach to this study. Moreover, in the deductive approach, there is a need for both the dependent and the independent variables. The dependent variable in this research is oil prices while the independent variable is the real GDP of the various countries with money supply, the rate of inflation and interest rate being the controlling factors.

3.3 Research strategy

The strategy chosen for implementation is the experimental strategy, which allows the study of the precise association between few variables that are studied in an intense manner by use of quantitative methods of analysis.The intention is to come up with generalized statements that have their application in real life circumstances (Hoe and Hoare, 2013). In this research, the variables examined are only two with three controlling factors. Furthermore, data concerning the variables are collected from real and measured figures. The advantage of this strategy is that the extension into situations of real life help in accomplishing greater realism and decreasing the degree to which circumstances can be criticized as being false.

3.4 Sample and sampling

This research does not employ probability methods of sampling that are known for quantitative studies, but rather utilizes non probability methods in which the countries to be examined are chosen by means of certain qualifications based on established facts, also known as judgment sampling. The research particularly focuses on developing African nations that are oil exporters. This helps bring out the uniqueness of the research given that the relationship between oil price shocks and macroeconomic variables have been studied since the pioneering work of Hamilton in the 80s. Among the developing African countries that export oil, six of the top ten exporters are settled upon with Angola being excluded due to theunavailability of data. The countries, therefore, considered include Egypt, Nigeria, Sudan, Libya, Algeria and South Africa. The sampling time frame spans from January 1985 to December 2013. The period is chosen so as to incorporate the effects of the most recent economic crisis.

3.5 Data collection methods

Given the types of variables sought in this study, the collection of the data as restricted to secondary methods. This includes the pooling of metadata from varied databases including the OECD, World Bank and the US energy information Administration (EIA). From the first database (OECD), all the values for South Africa were gathered being that it was the only country whose data was complete and available in the database. The data for the other countries was collected from the World Bank database. The EIA website was used for the sole purpose of obtaining data on the yearly price of crude oil. The reason for choosing these three databases is to enhance the validity and reliability of the data. The model employed is the VECM, an adaptation of the VAR model, with which data was analyzed stage by stage through the use of the STATA software.

3.6 The model

The fundamental model for this research is the vector autoregressive model (VAR), which is used especially for research concerning oil price shock-macro economy relationship. The VAR model of order X considered is:

Is regarded as an vector of endogenous variables, while Yt-I is taken as the subsequent lag term of order i. is a matrix of autoregressive coefficients of vector Yt-I for C is regarded as a intercept vector for the VAR model. Lastly, is taken as a vector of the white noise process.

Contrary to other researchers that employ the VAR model directly, this research is inclined to use either SVAR or VECM that gives a chance for the existence of lagged and contemporaneous interconnection between various variables. All the variables in a series are considered. Given that this research includes the analysis of six countries, the variables are separately considered for each country. The series is regarded as levels rather than rates of growth. This approach was selected because it enables the performance of innovation accounting, including the use of impulse response functions (IRF) for the purpose of examining the manner in which a single standard deviation shock in the oil price variable’s error term shock affects endogenous variables in the model. It also helps in the determination of the proportion of the variance of the forecast error of a certain variable that is a result of the oil shock.

To choose either SVAR or VECM order of integration and the presence of cointegration among the variables is used. In first place, an investigationof the presence of stationary properties among the variables using the Augmented Dickey-Fuller (ADF) test is conducted. In the case that all the variables give the result of I(0), the SVAR is preferred while if there is I(1), an examinationof the presence of cointegration using the Johansen procedure is performed . In the case that cointegration is detected, it is incorporated through the use of the vector error correction model (VECM) given that omitting it constitutes misspecification error. The VECM is obtained by transforming VAR, which yields:

,

And η and β refer to the adjustment matrix and the cointegration matrix. There are five endogenous variablesused in the following order: oil price, money supply, interest rate, inflation and GDP throughout the analyses for each of the countries. The study majorly focuses on two variables: real GDP and the real price of oil. The other variables are used for the purpose of incorporating the effect of low price shocks on GDP; inflation is regarded because of its ability to filter through the monetary policy.

Following the estimation using the chosen model, numerous tests are performed, including the Lagrange Multiplier (LM) test which helps in determining the existence of autocorrelation of residuals, Jarque-Bera which test for normality of residuals and the test for the stability of Eigenvalues. Following the success of these tests, innovation accounting using the IRF tests iscarried out, which helps in further interpreting the results.

Chapter 4: Results

This chapter examines the trend in the oil price as well as the VAR tests that provide the relationship between the real GDP and oil price volatility with the other independent variables used as mediating factors. This leads to the conclusions about the relationships realized and the behavior of the variables in the short term and in the long term.

4.1 The trend in oil price

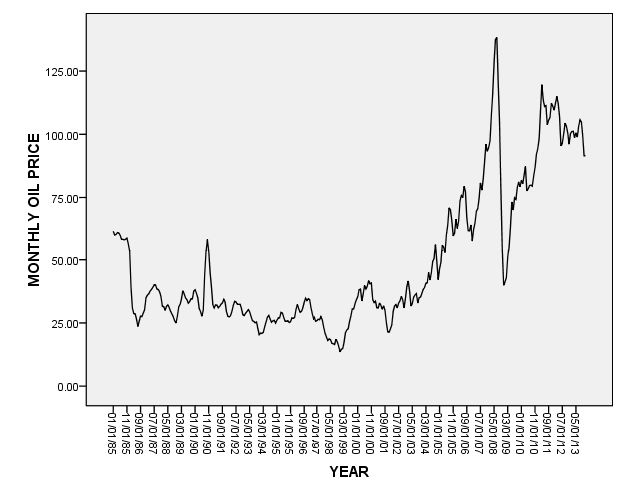

From the graph, it is apparent that the price of oil sharply rose after 2001 but experienced a sharp decline in 2009 after which it regained a sharp rise and is currently in decline although the decline is not as sharp as the previous declines. The 2009 decline can be attributed the world financial crisis, giving a premature implication that oil price shocks have a relationship with major economic downturns. Indeed, such a pre-emption is supported by Hamilton, who, according to the literature discussed, realized that the oil price shocks had a relationship or rather contributed to the financial crises with the exception of one in the period spanning the 1940s. A pictorial representation of the shocks is presented in the figure 4.1.

Figure 4.1: The trend of yearly oil price

4.2 Pre-test estimations of the model

The analysis begins by checking the stationary attributes of the data by using the augmented Dickey Fuller unit root tests. The null hypothesis for the test is that the variables have a unit root and the alternative hypothesis is that a process that is stationary produced the variable.

| Variable | South Africa | Algeria | Egypt | Libya | Nigeria | Sudan |

| Yearly real oil price | 0.8632 | 0.8632 | 0.8632 | 0.8632 | 0.8632 | 0.8632 |

| Interest rate | 0.3307 | 0.0017 | 0.0458 | 0.7492 | 0.0000 | |

| Money supply | 0.9176 | 0.4195 | 0.6542 | 0.6101 | 0.0499 | 0.4597 |

| Inflation | 0.1854 | 0.5087 | 0.2261 | 0.0374 | 0.1242 | 0.2762 |

| GDP | 0.9831 | 0.9951 | 1.0000 | 0.7316 | 0.9976 | 0.9856 |

Table 4.1: The results MacKinnon approximate p-valueof the Dickey-fuller test for stationary

From the results, the values of interest rate have significance for the data of Nigeria, Egypt and Algeria while those of inflation has significance for Libya. The implication is that the null hypothesis can be rejected for some variables while for the rest, the null hypothesis are adopted. Therefore,it can be concluded that all the variables with the exception of the rate of inflation and interest rate have unit roots leading to the use of VEC model. The level of significance was considered for critical values at 1%, 5% and 10%.

Given that a series at lag 1 is used, there is no need proceed to SVAR estimation.Therefore,it is checked whether there is long-termequilibrium (cointegration) between various variables, which is a condition that has to be met for the construction of VECM. Before then, the number of lags that ought to be included is established by using lag order selection statistics. The test returns Akaike’s information criterion (AIC), Hanna and Quinn information criterion and Schwarz’s Bayesian information criterion (SBIC) for order 1 through to the maximum lags. The results are indicated in the table 4.2.

| Country | Lag | p | AIC | HQIC | SBIC |

| South Africa | 0 | 70.2352 | 70.291 | 70.4288 | |

| 1 | 0.000 | 65.3699 | 65.6486 | 66.3377* | |

| 2 | 0.002 | 65.1538 | 65.6555 | 66.8958 | |

| 3 | 0.000 | 64.5487* | 65.2733* | 67.0649 | |

| Algeria | 0 | 5.8e+25* | 79.6597 | 79.832 | |

| 1 | 0.000 | 73.5325 | 73.9505 | 74.9842* | |

| 2 | 0.015 | 73.8163 | 74.5826 | 76.4776 | |

| 3 | 0.000 | 72.4949* | 73.6097* | 76.366 | |

| Egypt | 0 | 77.9716 | 78.0412 | 78.2135 | |

| 1 | 0.000 | 71.8928 | 72.3108 | 73.3444 | |

| 2 | 0.000 | 70.8352 | 71.6016 | 73.4965 | |

| 3 | 0.000 | 68.7168* | 69.8315* | 72.5879* | |

| Libya | 0 | 80.1756 | 80.2452 | 80.4175 | |

| 1 | 0.000 | 74.9863 | 75.4043 | 76.4379* | |

| 2 | 0.000 | 73.8347 | 74.601* | 76.496 | |

| 3 | 0.000 | 73.4904* | 74.6051 | 77.3615 | |

| Nigeria | 0 | 84.8609 | 84.9306 | 85.1029 | |

| 1 | 0.000 | 80.2486 | 80.6666 | 81.7002 | |

| 2 | 0.000 | 79.5371 | 80.3035 | 82.1985 | |

| 3 | 0.000 | 77.742* | 78.8567* | 81.6131* | |

| Sudan | 0 | 72.9538 | 73.0096 | 73.1474 | |

| 1 | 0.000 | 69.176 | 69.4546 | 70.1437* | |

| 2 | 0.000 | 68.4189* | 68.9205* | 70.1608 | |

| 3 | 0.000 | 68.6406 | 69.3652 | 71.1568 |

Table 4.2: Criteria for lag selection

From the results, it is apparent that for South Africa, the majority of the tests choose 3 lags, similar to Algeria, Egypt, and Nigeria while for Sudan the majority of the tests choose 2 lags and for Libya, each of the tests chooses different lags but three lags are settled upon. In the next test (cointegration) the number of cointegratingrank for the VEC test chosen is found out. The results of the test are indicated in the table 4.3.

| South Africa | Algeria | Egypt | |||||||||

| Rank | Trace | α=5% | Trace | α=5% | Trace | α=5% | |||||

| 0 | 72.9117 | 47.21 | 131.5986 | 68.52 | 144.1662 | 68.52 | |||||

| 1 | 34.4718 | 29.68 | 73.9992 | 47.21 | 80.9471 | 47.21 | |||||

| 2 | 12.8635* | 15.41 | 33.0197 | 29.68 | 39.0451 | 29.68 | |||||

| 3 | 0.1108 | 3.76 | 13.0036* | 15.41 | 18.1583 | 15.41 | |||||

| 4 | 3.8234 | 3.76 | 2.7217* | 3.76 | |||||||

| Libya | Nigeria | Sudan | |||||||||

| Rank | Trace | α=5% | Trace | α=5% | Trace | α=5% | |||||

| 0 | 114.3596 | 68.52 | 136.0676 | 68.52 | 61.5050 | 47.21 | |||||

| 1 | 70.9038 | 47.21 | 60.9475 | 47.21 | 26.9866* | 29.68 | |||||

| 2 | 44.5359 | 29.68 | 21.0898* | 29.68 | 5.5963 | 15.41 | |||||

| 3 | 25.4304 | 15.41 | 8.2708 | 15.41 | 0.7891 | 3.76 | |||||

Table 4.3: The results of the Johansen test for cointegration (VECM, 3 lags)

From the trace statistics, it can be seen that the null hypothesis which indicates that the number of distinct vectors of cointegration is less than or equal to four cannot be rejected given that the trace statistic is larger than that of the Eigen value at 5% critical value for Egyptand Libya but the alternative hypothesis is adopted in the remaining countries. The conclusion arrived at is that the final number of long run equilibrium for inclusion in the VECM with three lags is three for Egypt, Libya and Sudan while the rank chosen for South Africa, Algeria and Nigeria are four. The rank in Sudan is set at three because the variables are fewer and therefore the maximum allowable rank is three.

4.3 Post test estimations of the model

Following the VEC model estimation, numerous tests areexecutes in order to find out the trustworthiness of the model. First, the Lagrange-multiplier (LM) for testing the autocorrelation of the residuals is carried out. The null hypothesis indicates that the residuals are not auto-correlated at various lag orders. The results are displayed in the table 4.4.

| Lag | Prob>chi2 | |||||

| South Africa | Algeria | Egypt | Libya | Nigeria | Sudan | |

| 1 | 0.00228 | 0.31357 | 0.49512 | 0.67781 | 0.80835 | 0.52945 |

| 2 | 0.24643 | 0.70023 | 0.18860 | 0.55675 | 0.25821 | 0.32020 |

| 3 | 0.45816 | 0.59095 | 0.71352 | 0.07474 | 0.12291 | |

| 4 | 0.92781 | |||||

Table 4.4: The results of the LM test for the autocorrelation of 3-lagged VECM test

Given that the results show that the values of significance are less than 0.05 for the first lag for South Africa, the null hypothesis is rejected and the alternative hypothesis that the residuals are auto-correlated up to the third lagis adopted. The implication is that the coefficients have inefficient estimates and therefore distorts the procedure for testing a hypothesis by means of wider levels of confidence. Nevertheless, the residuals for the results for other countries show no autocorrelation.

TheJarque-Bera test is proceeded with to test the normality of the residuals. The null hypothesis is that the residuals are normally distributed. The results are shown in table 4.5.

| Equation | Prob>chi2 | |||||

| South Africa | Algeria | Egypt | Libya | Nigeria | Sudan | |

| Real Yearly oil price | 0.97322 | 0.06728 | 0.99901 | 0.25686 | 0.00180 | 0.00805 |

| Interest rate | 0.07023 | 0.90998 | 0.44045 | 0.00001 | 0.48288 | |

| Money supply | 0.62243 | 0.71967 | 0.10580 | 0.69319 | 0.67034 | 0.63418 |

| Inflation | 0.53185 | 0.69005 | 0.56101 | 0.31729 | 0.66935 | 0.00000 |

| GDP | 0.85524 | 0.37298 | 0.41224 | 0.85200 | 0.38342 | 0.47834 |

| ALL | 0.63956 | 0.53602 | 0.52616 | | 0.00075 | 0.06173 | 0.00000 |

Table 4.5: Normality test for 3-lagged VECM using Jarque – Bera test

The results show that the residuals for variables in some countries are normally distributed while others are not. This implies that the procedure for testing the hypothesis needs to be carried out with caution for certain countries and variables.According to Morana (2013), this is a phenomenon regarded as common and does not lead to critical distortion of the final results.

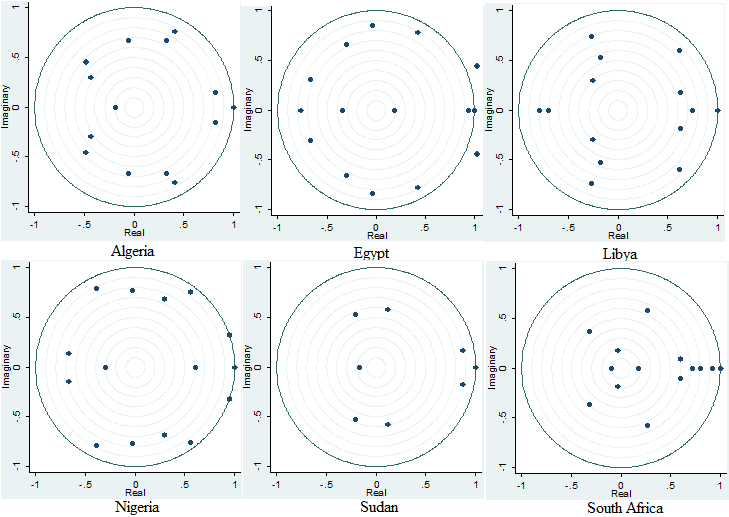

Further checks on whether the model satisfies the conditions for the stability of Eigenvalues are conducted. The results are displayed in the figure 4.2.

Figure 4.2: The Eigen stability circle

From figure 4.2, with the exception of the values for Egypt, the values for all the other countries are within the unity circle giving the implication of stability.

4.4 Short run and long run relationships between Oil price shock and GDP

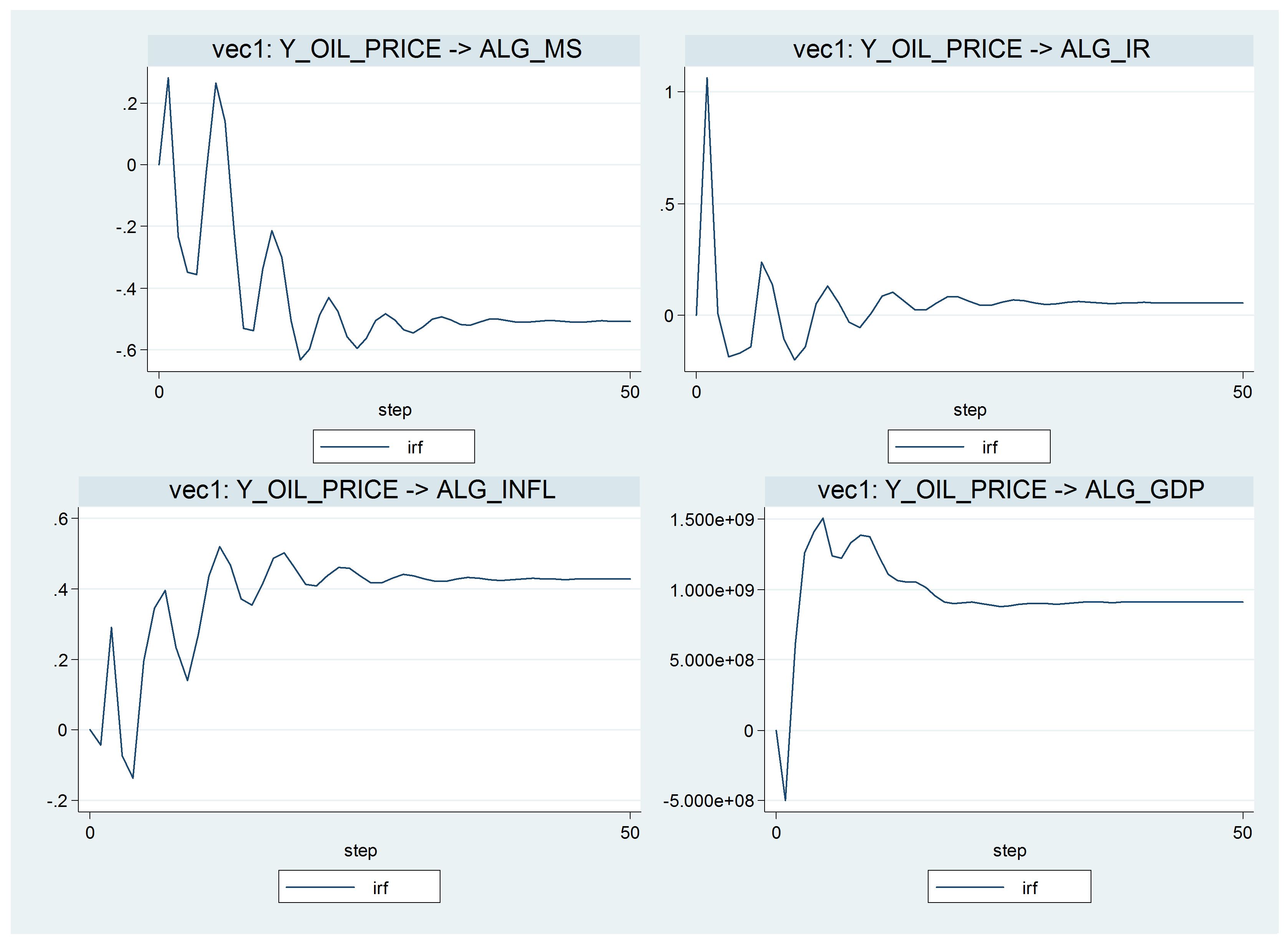

The last tests performed are the IRF impulse tests for the results of various countries. This helps in knowing the short term and long term behavior of various variables with the changes in oil price. Figure 4.3 shows the behavior of output in Algeria. From the results, it can be seen that in the short run, there is a sharp decline in GDP followed by a sharp rise and long term stability. The effect of oil price shock has an upward oscillating effect on the rate of inflation with the long run result being higher inflation. Interest rates on the other hand sharply increase and decline in the short term and returns to its initial point in the long run. The effects of the oil price shock on GDP and other macroeconomic variables seem to be a result of the injection of money supply following the reduction of oil prices. Nevertheless, this is done at the expense of rising inflation.

Figure 4.3: IRF with the impulse being the oil price in Algeria

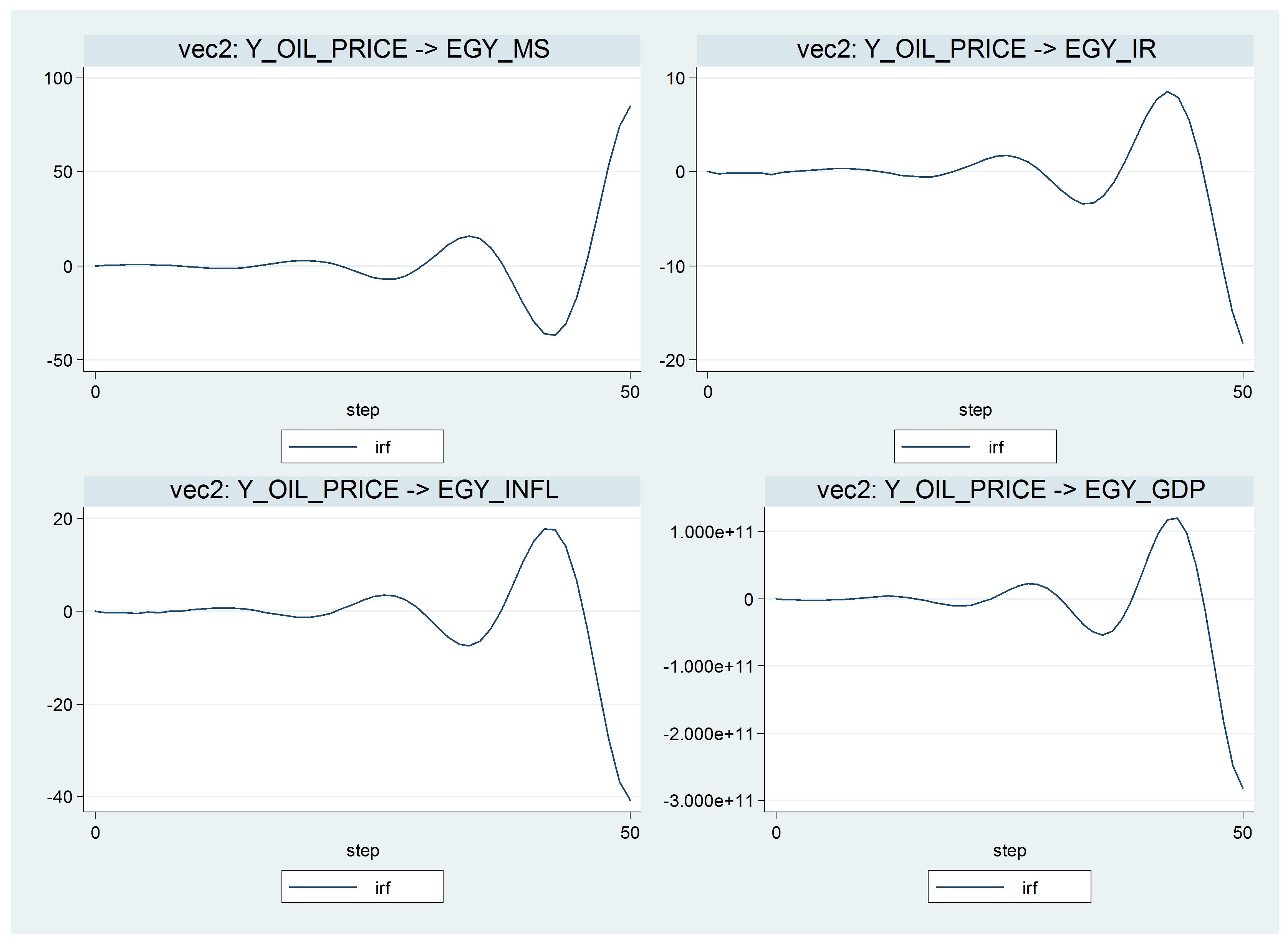

The results for Egypt are displayed in the figure 4.4. From the results, it can be seen that in the short run the country experiences a stable real GDP, but seems to have a sharp decrease in the long run which is accompanied by sharp decreases in both interest rates and inflation. This seems to be caused by the injection of money supply into the economy as a result of its decrease. This could also be caused by some exogenous variables given that in this country, the Eigenvalues did not indicate stability. Further, Egypt has experienced political unrest, which may have decreased output and not the prices of oil.

Figure 4.4: IRF with the impulse being the oil price in Egypt

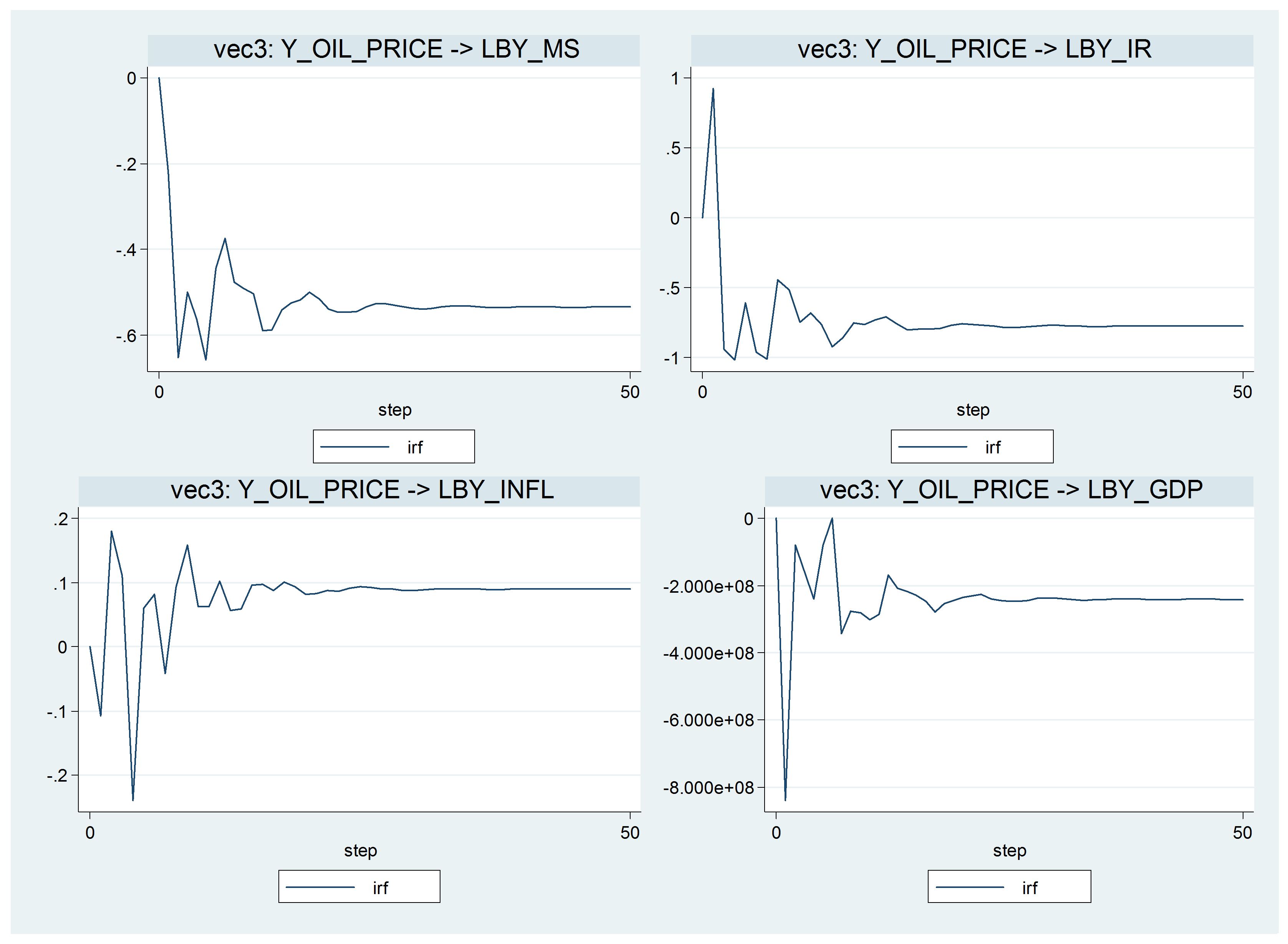

From the results displayed in the figure 4.5, it can be seen that in the short run, Libya experiences volatility in all the macroeconomic variables with no sign of government mediation. After two sharp declines in money supply, the injection of money supply into the economy results in stability of macroeconomic variables in the long run. Nevertheless, this late injection leads to lower GDP and inflation with high interest rates in the long run.

Figure 4.5: IRF with the impulse being the oil price in Libya

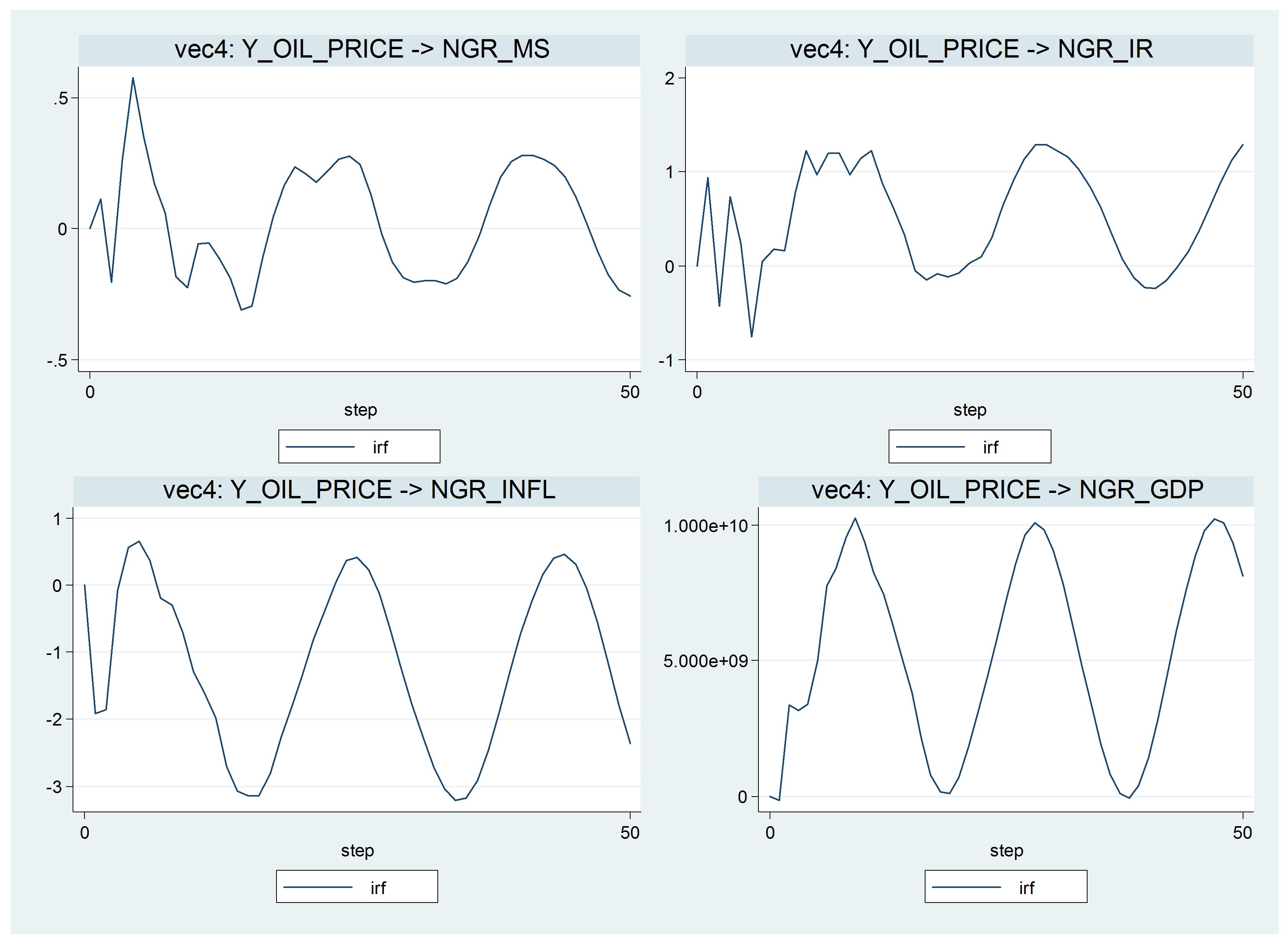

As for Nigeria, the injection of money supply in the economy following its sharp decline with the regulation of interest rates as showedby figure 4.6 results in a cyclical effect on both the rate of inflation and GDP in the long run.

Figure 4.6: IRF with the impulse being the oil price in Nigeria

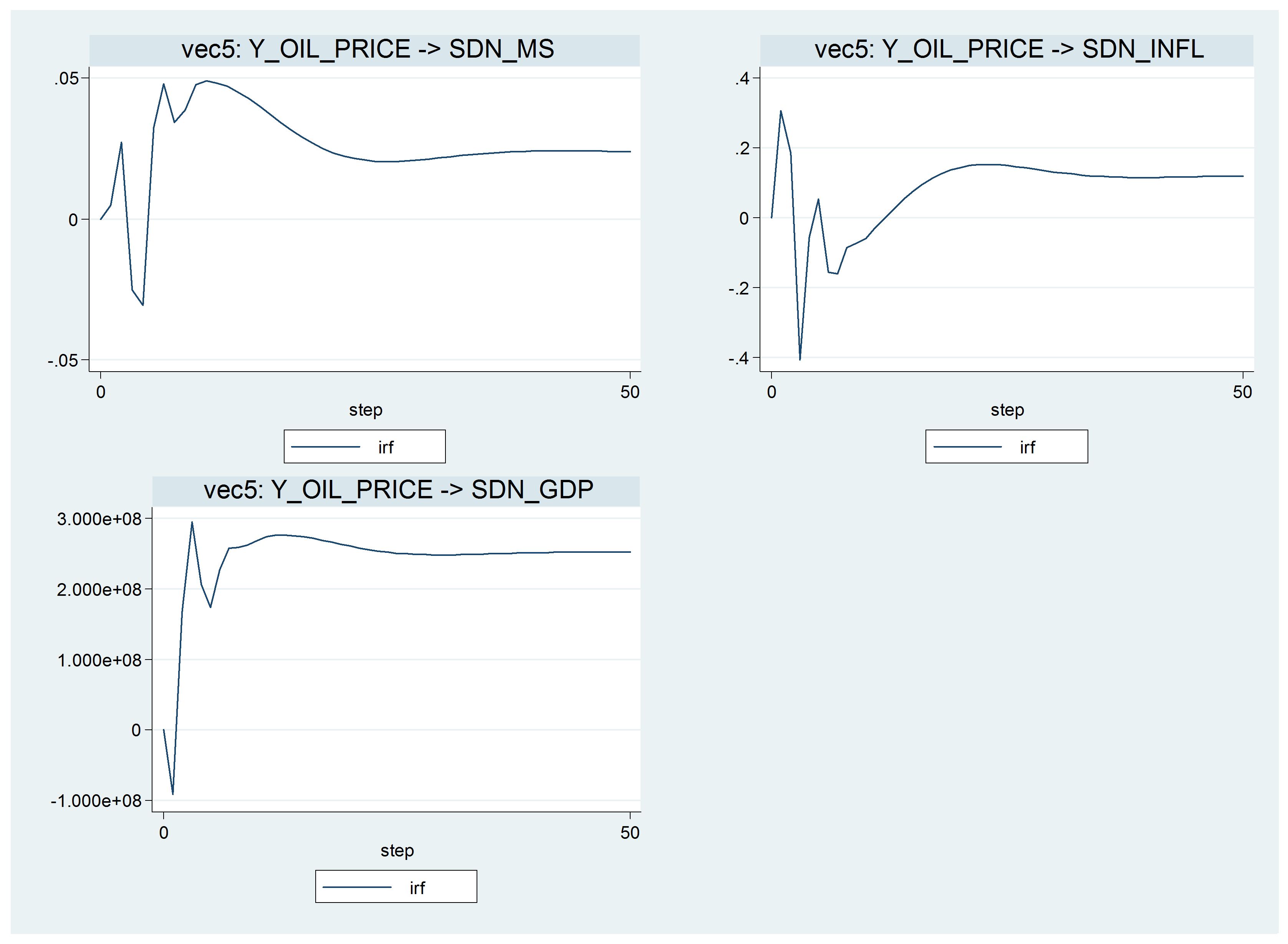

Sudan on the other hand, experiences a rise in GDP in the short run following the injection of money into its economy that comes after its sharp decline of the money supply. This causes sharp disturbances on the rate of inflation with all the variables permanently settling at a higher rate in the long run. The data for the country’s interest rate was not available.

Figure 4.7: IRF with the impulse being the oil price in Sudan

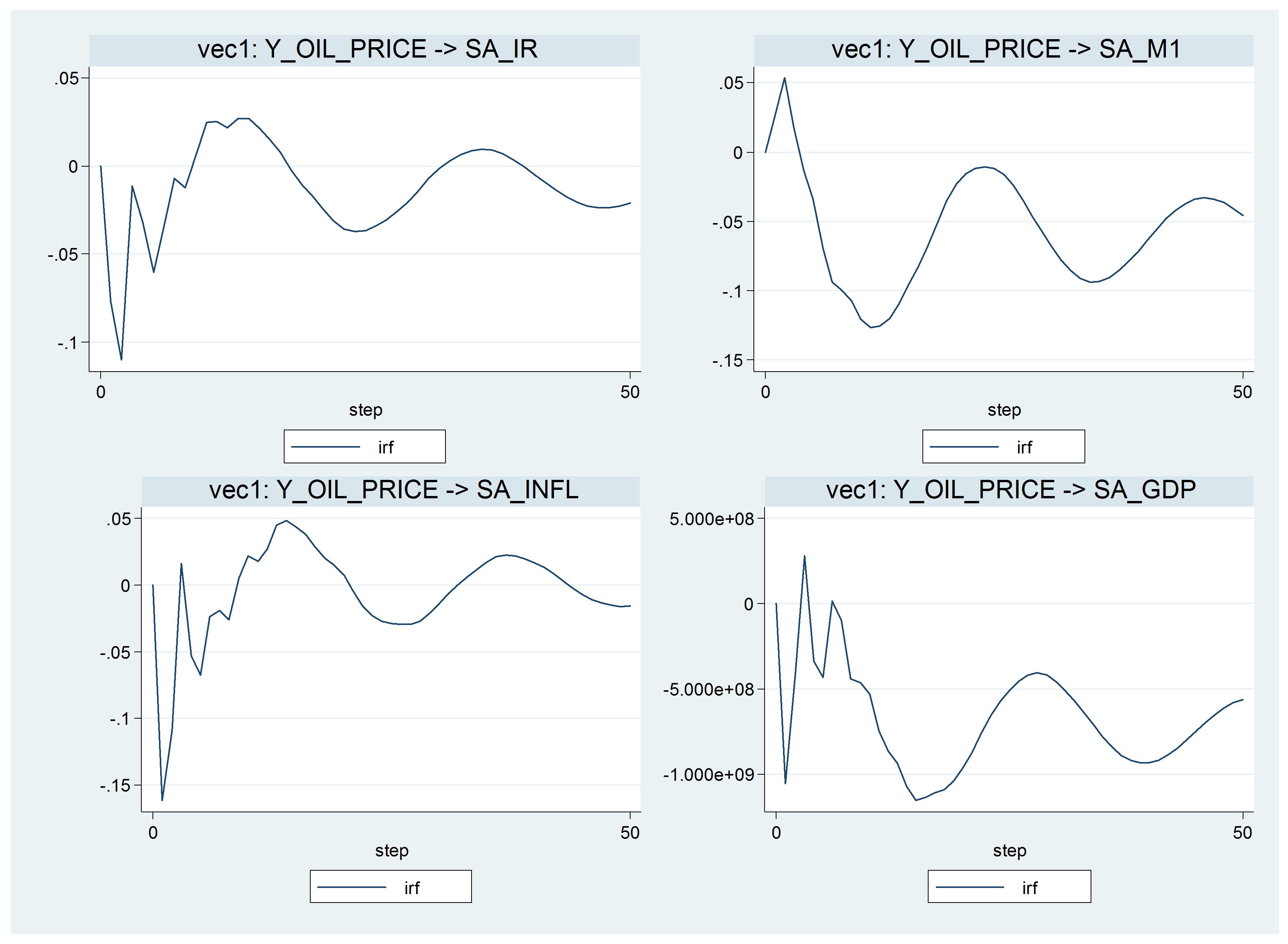

Lastly, South Africa seems not to intervene in terms of injecting money supply into its economy but by controlling interest rates. This leads a short run disturbance in the rate of inflation and GDP but with cyclical movements in the long run for all the macroeconomic variables.

Figure 4.8: IRF with the impulse being the oil price in South Africa

The results of the various African nations studied here, show that in the short term, there generally was volatility in the macro- economic structure. This further resulted in the intervention by government, with South Africa being the exception. The critical element to the government intervention was the injection of money into the economy by the government due to changes in oil prices. However, this had varying results on the macro- economic aspects of different countries in the long term. For example, Egypt had a decrease in interest rates and inflation. Libya faced a low GDP growth and increase in interest rates. Nigeria on the other hand had an effect which resulted in low interest rates and a cyclical effect on inflation and GDP. Sudan, however, had high inflation rate. The results therefore imply that oil price shocks do affect the economies of countries, especially the developing oil export countries. However, the results vary from one country to another and it is therefore important to understand the specificity of these economies. The empirical data therefore suggests a contrary conclusion to theoretical studies which presume the uniformity of the implications of oil price shocks on the economies of different countries. The realty to the contrary suggests that despite the fact that there are effects at the macro- economic levels, these are specific to countries and any research is to be conducted within the context of specific countries and accordingly conclusions are to be drawn. Similar findings pertaining to country specific effects have been postulated by Iwayemi and Fowowe (2011) and Ali, Huson and Wadud(2011).

Chapter 5: Conclusions and recommendations

The aim of this research was to investigate the impact of oil price shocks on the macroeconomy of oil exporting countries with the specific objectives being to investigate the current trend of oil price movements and to investigate the relationship between oil price shocks and macroeconomic performance for African oil exporters. The first objective was to establish that the trend in oil price has continued to vary greatly with downward shocks deepening but not at the level of the previous deeps. This means that with the continuous rise, even the sudden price decreases in the future may not measure up with the current high prices.

From the analyses shown, it is evident that an attempt to answer all research questions has been made. Particularly, It wasobserved that during the period considered, the rapid rise in oil prices has a short term rise in the GDP followed by a continual decline, increase, stability or a cyclical effect. The variation in the long run effect on output of the various countries is dependent on the amount of money injected into the economy and what level the injection occurs. Countries that inject money into the economy over a period experience a settlement of their GDP at higher rates while that those that inject money into their GDP at once following the decline of oil prices experience a cyclical effect in their macroeconomic variables in the long run. Countries that do not inject money at all, their GDP experiences volatility of the macroeconomic variables in the short run with the GDP settling at lower levels.

Given the observed variable dynamics, the conclusion drawn is that oil price transmission to the real economy takes place through cost and effects of upward demand. Particularly, demand effects are attributed to the short run, approximately three months to four months after the initiation in the oil price shock with the symptoms being the disturbance in the level of inflation, and increased GDP in comparison with long run, which takes place in approximately 24 months. The major reason behind this is the drop in the aggregate demand, which occurs following the accomplishment of the reduction in cost effects, a sharp increase in the monetary supply (M1) followed by the reduction in the same which comes from the increase in the rate of interest. Further, the long run effect following the disturbance depends on the government reaction following a sharp decline of the money supply. Generally, this research has established that the economy of Developing African countriessuffer or benefit more in the long term depending on their reaction shortly after the oil price shocks. This conclusion finds its support in the results of Al-Abri (2013).

Decreasing interest rates and fast rise in the money supply in the short run leads to the conclusion that the governments of the developing African exporters have to pump liquidity into the economy within a period of time for the purpose of stimulating the aggregate demand. This provides the reason for the disturbances ininflation and settlement of GDP at higher levels in the long run. Therefore, governments choose to sustain the levels of output the opportunity cost being disturbances in the levels of inflation. Same as the theoretical knowledge, this research realizes the direct effect of oil price on GDP, which in the theoretical sense should go beyond cost and the downward effects of demand and lead to the increase in inflation. This research observes the cyclical effect of second round inflation only in one country, which seems to pump liquidity into the economy instantly following its reduction.

This research did not consider numerous other oil exporting countries like Angola that is regarded as the largest oil producer. It also did not take into account upcoming exporters, but are still net importers. Future research should consider all African exporting countries.

References

Al-Abri, A. S. (2013). Oil price shocks and macroeconomic responses: does the exchange rate regime matter? OPEC Energy Review, 37 (1), 1-19.

Ali, A. Huson J., Wadud, I.K.M. (2011). Role of oil price shocks on macroeconomic activities: An SVAR approach to the Malaysian economy and monetary responses. Energy Policy, 39 (12), 8062-8069.

Barnham, C 2012, ‘Separating methodologies?’ International Journal of Market Research, vol. 54, no. 6, pp. 736-738.

Bernanke, B. S., Gertler, M. & Watson, M. W. (2004). Oil Shocks and Aggregate Macroeconomic Behavior: The Role of Monetary Policy. Journal of Money, Credit & Banking (Ohio State University Press), 36 (2), 287-291.

Berument, M.K., Ceylan, N.B. & Dogan, N. (2010). The Impact of Oil Price Shocks on the Economic Growth of Selected MENA Countries.The Energy Journal, 31(1), 149-177.

Bjørnland, H. C. (2008). Oil price shocks and stock market booms in an oil exporting country. Norges Bank: Working Papers, (16), 2-39.

Cavalcanti, T. &Jalles, J. T. (2013). Macroeconomic effects of oil price shocks in Brazil and in the United States. Applied Energy, 104, 475-486.

Chen, W., Hamori, S &Kinkyo, T. (2014). Macroeconomic impacts of oil prices and underlying financial shocks.Journal of International Financial Markets, Institutions & Money, 29, 1-12

Chuku, C. A. (2012). Linear and asymmetric impacts of oil price shocks in an oil-importing and -exporting economy: the case of Nigeria. OPEC Energy Review, 36 (4), 413-443.

Du, R Y & Kamakura, W A 2012, ‘QuantitativeTrendspotting’, Journal of Marketing Research (JMR), vol. 49, no. 4, pp. 514-536.

Filis, G. &Chatziantoniou, I. (2014). Financial and monetary policy responses to oil price shocks: evidence from oil-importing and oil-exporting countries. Review of Quantitative Finance & Accounting, 42 (4), 709-729.

Ghosh, N., Varvares, C. & Morley, J. (2009). The Effects of Oil Price Shocks on Output.Business Economics, 44 (4), 220-228.

Ghosh, S. &Kanjilal, K. (2014). Oil price shocks on Indian economy: evidence from Toda Yamamoto and Markov regime-switching VAR. Macroeconomics & Finance in Emerging Market Economies, 7 (1), 122-139.

Gómez-Loscos, A., Gadea, M. D. &Montañés, A. (2012). Economic growth, inflation and oil shocks: are the 1970s coming back? Applied Economics, 44 (35), 4575-4589.

Guidi, F. (2010). The Economic Effects of Oil Prices Shocks on the UK Manufacturing and Services Sectors.IUP Journal of Applied Economics, 9 (4), 5-34.

Hamilton, J. D. & Herrera, A. M. (2004). Oil Shocks and Aggregate Macroeconomic Behavior: The Role of Monetary Policy. Journal of Money, Credit & Banking (Ohio State University Press), 36 (2), 265-286.

Hoe, J & Hoare, Z 2012, ‘Understanding quantitativeresearch: part 1’, Nursing Standard, vol. 27, no. 15-17, pp. 52-57.

Hoe, J & Hoare, Z 2013, ‘Understanding quantitativeresearch: part 2’, Nursing Standard, vol. 27, no. 18, pp. 48-55.

Iwayemi, A. & Fowowe, B. (2011). Oil and the macroeconomy: empirical evidence from oil-exporting African countries. OPEC Energy Review, 35 (3), 227-269.

Iwayemi, A. & Fowowe, B. (2011). Impact of oil price shocks on selected macroeconomic variables in Nigeria.Energy Policy, 39 (2), 603-612.

Jimenez-Rodriguez, R. (2011). Macroeconomic Structure and Oil Price Shocks at the Industrial Level. International Economic Journal, 25 (1), 173-189.

Jiménez-Rodríguez, R. & Sánchez, M. (2009). Oil shocks and the macro-economy: a comparison across high oil price periods. Applied Economics Letters, 16 (16), 1633-1638.

Jiménez-Rodríguez, R. & Sánchez, M. (2012).Oil price shocks and Japanese macroeconomic developments.Asian-Pacific Economic Literature, 26 (1), 69-83.

Kilian, L. (2009). Not All Oil Price Shocks Are Alike: Disentangling Demand and Supply Shocks in the Crude Oil Market. American Economic Review, 99 (3), 1053-1069.

Morana, C. (2013). The Oil Price-Macroeconomy Relationship since the Mid-1980s: A Global Perspective.Energy Journal, 34 (3), 153-189.

NG, W. (2012). Oil Price Volatility and the Singapore Macroeconomy.Singapore Economic Review, 57 (3), 1-26.

Serletis, A. & Elder, J. (2011). Introduction to Oil Price Shocks.MacroeconomicDynamics, 15, 327-336.

Ushie, V., Adeniyi, O. &Akongwale, S. (2012).Oil revenue, institutions and macroeconomic indicators in Nigeria.OPEC Energy Review, 37 (1), 30-52. Mar2013

INSTANT PRICE

Get an Instant Price. No Signup Required

We respect your privacy and confidentiality!

Share the excitement and

get a 15% discount

Introduce your friends to The Uni Tutor and get rewarded when they order!